Trending Forward: Data Centers, The Cornerstone Of the Digital Age

Investing Insights from the Sustainable Equity Team

In brief

- The rapid expansion of artificial intelligence (AI) has significantly increased the demand for data centers, creating investment opportunities across the entire value chain.

- A significant upgrade to the physical digital infrastructure is essential for enhancing efficiency and scalability.

- Several challenges are delaying the expansion of data centers, including issues with power supply availability, resource bottlenecks, and high capital expenditures.

Technology

Data Centers

We invest in companies with meaningful exposure to economic tailwinds from longterm transitions that are affecting the global economy: demographics, environmental, technological and governance. The technology transition includes artificial intelligence, digitalization of the economy, and increasing connectivity and automation which are expected to transform industries, improve efficiency, and create new opportunities.

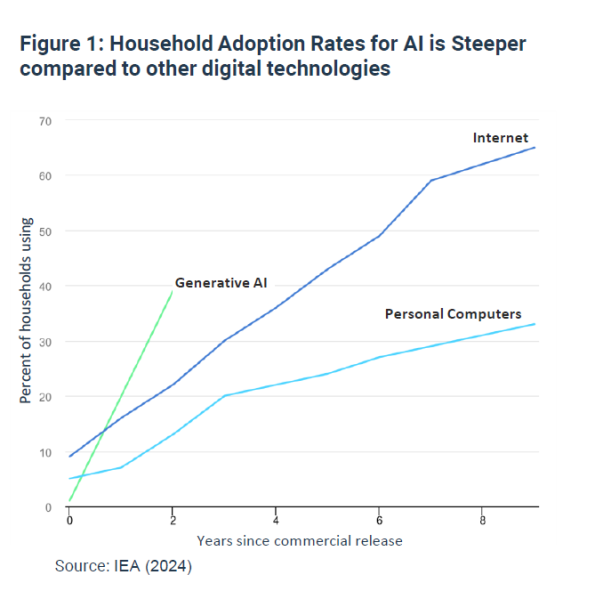

Technology, workplaces, and the economy are facing a significant transition driven by the rapid growth and adoption of artificial intelligence (AI). Critical to this transformation are data centers— the facilities that house the equipment that stores, processes, and distributes data for AI workflows. Over the past decade, data centers have experienced rapid growth, and there are no signs of slowing down. The increasing demand for generative AI as well as the next wave of computing is set to accelerate this growth.

While GPU chips often dominate discussions about AI, it’s important to look beyond the headlines to understand the many components that make up a data center. These facilities require substantial physical space and an array of infrastructure to operate effectively. There are two key physical layers of data centers known as white space and gray space. White space is generally dedicated to core IT equipment including servers and networking, and gray space refers broadly to the infrastructure-related surrounding areas including power, HVAC (heating, ventilation, and air conditioning), and building operations.

Demand for data center capacity in gigawatts has the potential to more than triple by 2030.1

Data centers are at an inflection point. To keep pace with the surging demand for data storage and processing, massive investment and innovation are required by companies who build, design, and operate data centers to stay ahead in the digital transformation we are experiencing.

Global data center market size was valued at USD 242.72 billion in 2024 and is projected to grow from USD 269.79 billion in 2025 to USD 584.86 by 2032.2

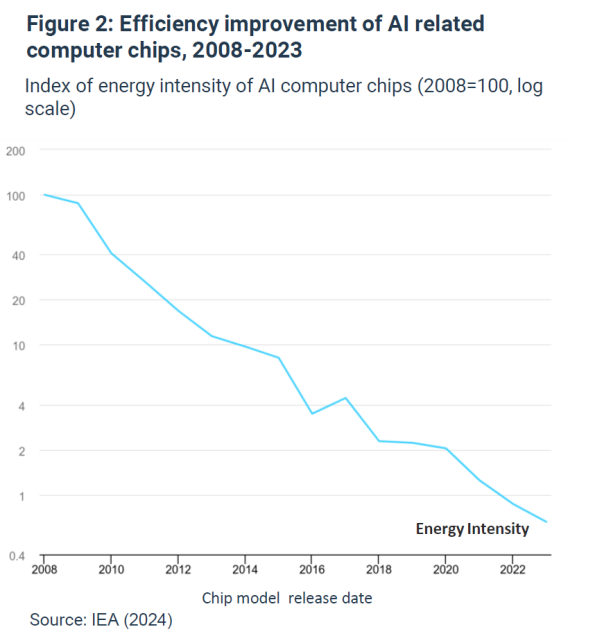

A significant upgrade of the physical digital infrastructure is essential. Not only do we need more data centers, but we need more efficient data centers. This will require investment in data processing and storage as well as the critical infrastructure components that support the technology such as electricity systems, cooling technologies, and advanced hardware. Companies across the value chain are investing in innovative solutions to continue to improve efficiency and scalability.

Companies across the value chain will need to invest $5.2 trillion into data centers by 2030 to meet worldwide demand for AI alone.3

There are several challenges delaying the expansion of the physical digital infrastructure in data centers. Access to and availability of power supply poses a significant hurdle. In other areas, resource bottlenecks have led to increased costs and time delays. Additionally, the high capital expenditure required for the build-out and the upgrades of data centers create a barrier for entry and a financial risk for many organiza-tions. As the industry addresses these challenges, new technologies are emerging across computing, electrical equipment, and cooling to drive efficiencies and reduce the energy consumption of data centers. These challenges are shaping the industry landscape and defining who

the leaders are in this transition.

As the demand for data center capacity continues to rise, those who prioritize efficient scaling, invest in innovative technologies, and establish resilient supply chains will emerge as leaders in this rapidly evolving market. The winners will not only be defined by their ability to meet immediate demands but also by their capacity to account and plan for the future of generative AI and the next wave of cloud computing. This process involves securing energy commitments along with the physical infrastructure.

Key Enablers

HYPERSCALERS: Cloud service providers that operate large data centers to support massive amounts of data processing, storage, and networking needs, enabling them to deliver cloud services efficiently and at scale.

MICROSOFT is a leader in the development of generative AI. A growing segment of the company’s offerings is cloud-based, contributing to 41% of its total revenues.4 In FY26, Microsoft is expected to grow capital expenditure by over 30%.5

SEMICONDUCTORS: Includes the compute components (including GPU, CPU, and ASIC), memory and storage solutions (such as high-bandwidth memory and NAND), connectivity chips, and power management integrated circuits (ICs) for data centers.

NVIDIA is the world leader in accelerated computing and leading developer of graphics processing units (GPUs) providing essential hardware for the development of AI. The company has over 80% of the market share in accelerated GPU chips.6

HARDWARE: Servers that house semiconductors, along with switches and networking equipment to facilitate communication between chips within the servers and to interconnect multiple servers. Additionally, optical fibers and cables are employed to transfer data efficiently across the infrastructure.

DELL TECHNOLOGIES is a leader in technology solutions, providing hardware, software, and services designed to optimize data center operations. Their offerings include servers, storage systems, and networking equipment, helping improve energy efficiency and scale IT infrastructure.

INFRASTRUCTURE - ELECTRICAL AND THERMAL EQUIPMENT: Electrical and thermal equipment represents the largest combined $ TAM within data centers. Electrical equipment includes power distribution units (PDUs), uninterruptible power supplies (UPS), and switchgear. Thermal equipment consists of cooling systems including the facility’s HVAC and direct-to-chip cooling.

HUBBELL specializes in manufacturing and selling electrical products and solutions essential for utilities, playing a vital role in grid modernization and electrification. The company also provides electrical infrastructure for data centers, focusing on energy efficiency to meet the growing demands of data center construction.

INFRASTRUCTURE - ENERGY AND POWER SUPPLY: A reliable energy supply is essential for the uninterrupted operation of data centers, encompassing the integration of utility power, energy storage, and onsite power generation systems.

NEXTERA ENERGY INC. generates, transmits, distributes, and sells electric power to retail and wholesale customers in North America. The company helps meet growing energy demand needs, including data centers, by operating long-term contracted assets with a significant focus on renewable generation.

Risk Management & Responsible Practices:

As the demand for AI continues to rise, so does the energy consumption of data centers. Global data center electricity consumption acounted for 1.5% of the world’s electricity consumption (415 TwH) in 2024 and is set to more than double by 2030 to 945 TWh.7 Additionally, with the expansion of digital infrastructure, there are significant other environmental risks emerging across the AI value chain, including increased carbon emissions, threats to biodiversity, and strain on water resources. To mitigate these risks, we tailor our engagement strategy to a company’s business model to focus on material climate impacts and promote best practices. Ultimately, our ambition is to promote and support the development of a sustainable digital economy that respects planetary boundaries. To achieve this, we have identified two themes for engagement on climate and AI: decarbonization of data centers and supporting the scaling up of renewable energy.

Shawn KUMAR

Senior Investment Analyst

Joseph TOSCANO

Equity Analyst, CFA*

1Source: McKinsey & Company. “AI power: Expanding data center capacity to meet growing demand.” (2024). The information provided reflects MIROVA’s opinion as of the date of this document and is subject to change without notice. The reported data reflect the situation as of the date of this document and are subject to change without notice. CFA® & Chartered Financial Analyst® are registered trademarks owned by the CFA Institute. The securities mentioned above are shown for illustrative purpose only and should not be considered as a recommendation or a solicitation to buy or sell.

2Source: Fortune Business Insights (2025)

3Source: McKinsey & Company “The cost of compute: A $7 trillion race to scale data centers” The securities mentioned above are shown for illustrative purpose only and should not be considered as a recommendation or a solicitation to buy or sell. The information provided reflects MIROVA’s opinion as of the date of this document and is subject to change without notice. The reported data reflect the situation as of the date of this document and are subject to change without notice.

4Source: Mirova

5Source: Mirova

6Source: Mirova

The securities mentioned above are shown for illustrative purpose only and should not be considered as a recommendation or a solicitation to buy or sell. The information provided reflects MIROVA’s opinion as of the date of this document and is subject to change without notice. The reported data reflect the situation as of the date of this document and are subject to change without notice.

7Source: International Energy Agency (IEA). The securities mentioned above are shown for illustrative purpose only and should not be considered as a recommendation or a solicitation to buy or sell. The information provided reflects MIROVA’s opinion as of the date of this document and is subject to change without notice. The reported data

reflect the situation as of the date of this document and are subject to change without notice.

A strategic component of long-term economic growthInvesting Insights from the Sustainable Equity Team

![[US] Mirova Global Equity Fund: impact report 2023](/sites/default/files/styles/visuel/public/2022-07/mirova-kv_multi_04-world-rgb_bd.jpg?h=efef00f5&itok=3u5kkmg3)

Discover the 2025 Impact Report for Mirova Global Equity Strategy.

The evolution and future of softwareInvesting Insights from the Sustainable Equity Team