Position paper: Environmental Market Instruments

This paper outlines Mirova’s position on the potential recourse to so-called “environmental market instruments” such as voluntary carbon credits and biodiversity credits/certificates.

Let’s take a step back

LEXICOLOGY

Carbon credits

A carbon credit is considered to be a unit equivalent to one tonne of CO2 avoided or sequestered. Carbon credits are awarded to greenhouse gas (GHG) emission reduction projects that meet certain criteria.

Project sponsors can sell their carbon credits to companies, local authorities or individuals who are voluntarily reducing their emissions and aiming for carbon neutrality.

For companies, this contribution strategy follows the completion of a GHG assessment and the implementation of a reduction plan. The carbon contribution is designed to offset residual, incompressible GHG emissions.

The existing methodologies tend to agree on 4 essential criteria:

- The project promoter must show that without the money from the sale of carbon credits, the project could not have been implemented and therefore would not have enabled carbon sequestration.

- The amount of CO2 avoided or sequestered must be quantifiable on the basis of a recognized methodology.

- Tons of CO2 sold as carbon credits must be verifiable and accounted for every year.

- Carbon avoidance or sequestration must take place over the long term

Projects eligible for the sale of carbon credits fall into two categories:

- Avoidance projects: developing renewable energy or using energy more efficiently;

- Sequestration projects: development of natural carbon sinks (forests, oceans, soils) or industrial sinks (machines that capture CO2 and store it in rock).

Biodiversity certificates/credits

Biodiversity credits/certificates are a new financial instrument that could play a pivotal role in contributing to a nature-positive economy.

While there is no firmly agreed definition yet, biodiversity credits can be described as a verifiable, quantifiable and tradeable financing instrument that rewards positive outcomes for biodiversity through the creation and sale of either land or ocean-based biodiversity units over a fixed period. With sufficient safeguards and high-integrity standards, credits can be used to finance actions that result in measurable improved outcomes for biodiversity, encompassing species, ecosystems, and ecosystem services.

Biodiversity credits can create positive value for business by reducing exposure to physical nature risks, keeping pace with regulatory changes, supporting positive nature outcomes aligned with consumer preferences, and securing access to competitive finance. Biodiversity credits are part of a company’s nature-positive journey, meaning they are an investment in nature’s recovery, not an offset for any damage done.

Complex by nature

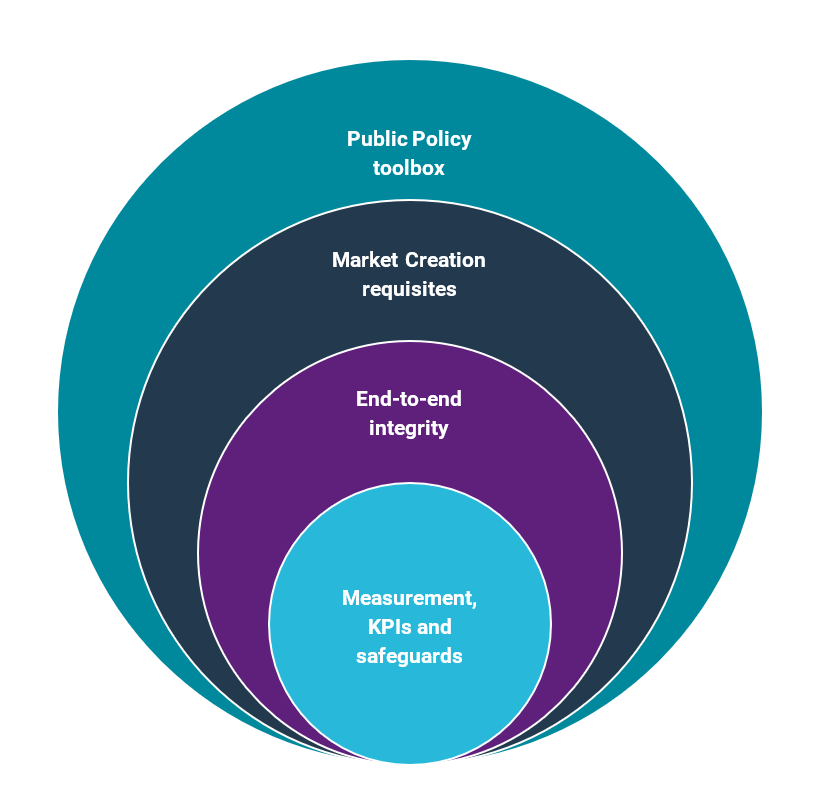

Environmental markets are complex by nature, with multiple entry points as well as pre-conceived ideas and controversies. It is critical to take a step back to consider the intricacies involved.

Based on Mirova’s participation to multiple working groups, conferences and debates on these topics, we have identified four intertwined topics:

Public Policy: one tool in the box

Several actions are needed

In order to fight climate change and biodiversity loss, global regulation needs to move forward on various aspects, from rules and norms to tax mechanisms and market-based instruments, to name a few.

In addition, multiple sources can be explored to mobilize more funding for nature and climate positive projects, which are often found in emerging economies, where the perceived risks tend to discourage private investors to get on board. Public, private and philanthropic money are proving to be complementary levers to channel more investment towards nature restoration and conservation.

Let’s be clear: carbon credits and biodiversity certificates are not meant to be silver bullets. They are useful instruments among many others to help transforming the economy into a more sustainable and inclusive model. These instruments are part of a broader effort to be taken by governments, public and private institutions, as well as by civil society organizations and individuals.

Recognizing that voluntary markets are only one piece of the puzzle is key to relieve part of the pressure. If criticism and scrutiny are always welcome constantly to improve the markets towards better practices, it should be up to reasonable expectations. Let’s be realistic about what such markets can bring while remaining vigilant at the way they will operate.

Voluntary is becoming mandatory

While voluntary commitments to climate and nature have been seen as an element of Corporate Social Responsibility (CSR) for many years, it is increasingly becoming a ‘must-have’ for many corporations and a key factor in a competitive environment. Voluntary commitments are often seen as less rigorous or less ambitious, but the reality is much more nuanced.

One often opposes voluntary to compliance market, or voluntary to mandatory commitment. However, there is a grey area where voluntary commitments become part of a regulated environment. For instance, in the carbon market, voluntary standards such as Verra or Gold Standard are recognized by compliance markets such as the Carbon Offsetting and Reduction Scheme for International Aviation (CORSIA) (covering the international aviation sector and piloted by the International Civil Aviation Organization, or ICAO). Similarly, reference to voluntary Net Zero commitments based, for instance, on the Science-Based Targets Corporate Net-Zero Standard and the related recourse to voluntary carbon credits need to be disclosed under the European Union's Corporate Sustainability Reporting Directive (CSRD)1 and the related reporting framework.

Voluntary standards are gradually becoming the norm and the frontier between voluntary and compliance market becomes blurred. As such, it seems more relevant to start referring to “Verified Carbon Credits” instead of “Voluntary Carbon Credits”.

The articulation between the Article 6 of the Paris Agreement2 and voluntary carbon markets (VCMs) is complex and subject to debates, as observed during the 28th Convention of Parties (COP28) in December 2023. In Dubai, Member States did not achieve a much-anticipated agreement on guidance for the operationalization of Article 6. Discussions and multilateral negotiations will continue in the forthcoming COPs. Meanwhile, VCMs have been subject to strong political support, joint declarations, and initiatives by leading standards to increase market integrity. Mirova supports the convergence between voluntary markets, which contributed to the development and consolidation of practices, and the operationalization of Article 6, in order to establish a more transparent and efficient carbon market. This could take the form of the recognition and approval of some voluntary standards’ methodologies under Article 6.

What does it take to shape a market?

Considerations on liquidity and fungibility

Any market needs liquidity to be efficient and to ensure that the price reflects the balance between both supply and demand of a given product/service, thus truly corresponding to a “market price”. But while liquidity requires some form of fungibility, it does not prevent specificity from being reflected into market compartments or sub-categories. An analogy with the wine market helps us to better understand these considerations.

No one can deny the existence of a global wine market. However, renowned wines and lower quality wines are not traded in the same way. Instead, there are a myriad of sub-markets within the global market, each distinctly shaped by the quality of its products, with room for specific price quotation related to such aspects as territory, grape variety, vintage, etc.

The existence of a wine market is therefore not linked to the setting of a single price for wine and the market is not fully fungible as prices differ depending on wine quality.

The same principle can be applied to environmental market instruments. Our perspective is that full fungibility is not required nor is it relevant. Attention must be paid to the specific quality of each underlying project. On the other hand, let’s not reject the recourse to market instruments: as is the case for the wine market, the opportunity is there to build an efficient, yet specialized market.

More generally, a market does not need any trading activities to exist. The market for renewable energy funding, with competition between banks and other types of investors to provide funding to underlying renewable energy projects, has led to a strong, well-financed sector. Similarly, one can aim for a competitive and efficient market to fund nature-positive projects.

Regarding market organization, we believe that creating a biodiversity certificate market can only succeed if the VCMs are improved. Improvement is happening already, as seen by the recent developments at COP28. Voluntary Biodiversity Markets can leverage such work and replicate what works.

The green bond market can also prove to be a relevant benchmark for voluntary markets development. 10 years ago, the Green Bond Principles (GBPs) were created by several banks, in conjunction with other market players (issuers, investors, auditors). They have enabled significant and healthy development of this market, and its extension to related innovations (social bonds, sustainability-linked bonds). They have become the benchmark and sole point of contact for regulators and public authorities (notably the European Union). The carbon and biodiversity credit markets share many similarities with the green bond market and could follow a similar path. For this approach to succeed, a consensus amongst market players and stakeholders is crucial to ensure legitimacy and to reach critical mass rapidly.

Focus on the International Advisory Panel on Biodiversity certificates

After the Summit for a New Global Financing Pact convened by French President Macron in Paris in June 2023 and six months after the adoption of the Global Biodiversity Framework (GBF), the UK and French governments launched the International Advisory Panel on Biodiversity Credits (IAPB) to drive the growth and scaling of high-integrity biodiversity credit markets. Co-chaired by Sylvie Goulard and Dame Amelia Fawcett, the initiative aims to galvanize international biodiversity credit markets.

The IAPB is operating as an independent and global initiative, bringing together expertise from all sectors, public and private, and building upon existing initiatives to contribute to the scaling up of investments through high integrity nature markets.

21 members of the UK-France government-initiated panel have been appointed, among them, representatives from International Union for Conservation of Nature, Science Based Targets Network and Taskforce on Nature-related Financial Disclosures. Mirova’s CEO Philippe Zaouati is part of the IAPB and co-chairs the Supply Working Group, alongside Pauline Nantongo, CEO of Ecotrust.

End-to-end Integrity: demand-side integrity matters as much as supply-side integrity

Supply-side integrity

Carbon standards have made significant progress over the past couple of years. In the wake of controversies raised by academic studies and press articles around doubtful calculations and methodologies leading to the generation of carbon credits, many initiatives have led to consolidated mechanisms to ensure a certain level of trust for given carbon standards. For instance, the Core Carbon Principles (CCPs), established by the Integrity Council on the Voluntary Carbon Market (ICVCM), are meant to provide safeguard and minimum requirements for carbon standards to be recognized in credible Net Zero initiatives.

During COP28, six independent crediting programmes joined forces to amplify the impact of carbon markets in accelerating mitigation efforts. Reports have also contributed to improving the integrity of the underlying projects, such as the comprehensive guidance on forest conservation shared by The Nature Conservancy.

On the biodiversity front, a number of consideration topics and initiatives have also emerged. Clear guidelines are needed from the outset to ensure a sufficient common denominator for increase the use of standards, with minimum requirements across the various standards. While some independent standards are emerging, such as Terrasos’ approach, other standards are being developed by entities already involved in the VCMs, including Verra and Plan Vivo Foundation.

Standards are needed but they are not enough: operators, developers, fund managers and investors must conduct their own analysis where relevant, in line with their respective roles and responsibilities.

Mirova’s extra layer of analysis and scrutiny to ensure integrity

To select underlying projects and ensure the quality of the supply and of the positive impacts generated on the ground, Mirova has developed its own policy and framework that leverages on international standards while adding specific criteria assessed by a solid team of ESG experts.

For carbon projects for instance, in addition to the basic requirement for any carbon standard which includes criteria such as quantifiability, reality, additionality, permanence, verifiability, etc., Mirova adds another layer of criteria including:

- carbon accounting consistency (calculations for carbon credit estimations must be based on robust literature, transparent assumptions and up to date methodology),

- social co-benefits (projects must – as much as possible – provide local communities with a fair benefit sharing scheme (e.g., % of carbon credit sales), livelihood improvement, capacity building and social programs,

- environment co-benefits (projects must ensure that the local biodiversity is well protected or regenerated within and outside the project’s boundary).

Demand side integrity: a call for a “just contribution”

In the carbon space, the concept of simple compensation and the related claim of carbon neutral products, flights, ingredients, company, etc. has become obsolete and is now subject to regulation: for example, the EU Parliament has recently adopted new regulations banning greenwashing and misleading product information.

The recourse to carbon markets should be part of a wider approach that takes into account the global strategy of any given company towards an alignment with its global Net Zero objective, based on science-based targets. For example, under the Science-Based Targets Corporate Net-Zero Standard, companies must disclose their direct emissions (scope 1) or indirect (scope 2 and 3) as well as their plan to reduce them, with specific milestones. Only alongside real reductions approved by the SBTi or similar Net Zero standards should the recourse to carbon credits be used to neutralize the residual or “hard to abate” emissions. In a way, this could still qualify as a form of compensation, but given all the prerequisite outlined above, a different word could be used for clarification.

For biodiversity credit markets, the principle of compensation is recognized in regulated or compliance markets as part of the “Avoid-Reduce-Compensate” hierarchy. But such principle for “no net loss” is often framed into strict rules meant to prevent the misuse of such credits.

Beyond the specifics of such compliance markets, the ability to reproduce the recourse to carbon credits under a transparent Net Zero strategy is being challenged by many stakeholders when it comes to biodiversity. We have been observing frequent calls to voluntary “contributions” which are not meant to be accounted for nor be part of any compensation mechanism and could be supported by philanthropy. While the principle of compensation bears the risk of maintaining business-as-usual for biodiversity credits buyers, we believe that the absence of any reference or any level of effort required by a company making a voluntary contribution might also prevent significant ambition for the market.

Mirova tends to support the principle of a “just contribution” that should be commensurate to the actual impacts of the given company. Reducing negative impacts needs to be the top priority. But recognizing positive contributions with specific criteria linked to the time horizon and the location of the contribution would still be required.

Such an approach is supported by other market players such as Pollination. Corporate commitments can leverage significant funding for nature, and initiatives such as the Science-based Target Network could lead to substantial amount of funding for nature, should game rules and related safeguards be clearly defined.

Mirova’s demand-side integrity policy

At Mirova, we have developed a demand-side integrity policy that prevents us from selling carbon credits to entities that do not have a clear net zero strategy compatible with science. Mirova is therefore setting criteria to sell or deliver carbon credits only to responsible companies, in order to ensure we do not contribute to unfair green marketing practices, such as claim positive impacts from the use of carbon credits while doing significant harm on other environmental or social objectives through their activities or practices, or use carbon credits in its climate strategy without being consistent with what climate science requires to really contribute or align their activities to a <2°C world. We also engage with our partners and companies we invest in to sell carbon credits to responsible companies, and therefore require that a similar kind of demand-side integrity policy is set. It also means that we expect the same engagement for any company that would co-invest in a project where Mirova is involved.

Measurements, indicators and safeguards: combining complexity and efficiency

Methodologies for defining and quantifying high-quality carbon credits and biodiversity certificates are evolving rapidly. This has resulted in a wide range of terminologies and approaches. Navigating and evaluating the merits of alternative paths can be challenging, particularly considering the ongoing debates on terminology (with references to both “certificates” and “credits”) and the specific “units” used to represent biodiversity uplift as a result of project activities.

However, there is a growing consensus that methodologies for quantification of biodiversity uplift will need to be sufficiently flexible to cater for a wide variety of biomes and biodiversity. As for the unit of quantification, Mirova supports a vision combining simplicity with units reflecting both spatial extent and increase in biodiversity/ecosystem condition.

Mirova’s experience with IPLCs

Mirova has already developed nature protection projects with Indigenous communities. For instance, as part of a primary forest protection in Peru, Mirova has provided long-term financing to a local NGO working with seven indigenous communities to address the drivers of deforestation of the region and consolidate sustainable land use. The communities are heavily involved in the protection of the forest and are trained by the local NGO implementing the project. The project aims to impact indigenous livelihoods through the development of sustainable forest related value chain and jobs creation. The project involves working closely with indigenous communities to help them develop socio-economic activities. It has created an Indigenous Company to support them with an emphasis on women. The experience shows that solid social engineering and local knowledge is needed to design and build the project, and that it requires expertise, time and energy.

Mirova’s view is that methodologies for calculating biodiversity uplift need to exhibit in-built flexibility but within a clearly defined framework or “minimum requirements”. Several of the existing biodiversity credit methodologies (e.g., Wallacea Trust, Verra’s SD VISta Nature Framework) reflect recognition of the diverse values of nature within their approaches to quantification of a biodiversity or nature “unit” through adoption of a “basket-of-metrics" approach. This, combined with the flexibility to apply a combination of a rapidly increasing range of techniques to collect the required biodiversity and ecosystem data is considered essential. Implementation of this flexible approach in a way that is considered robust, consistent and reliable requires participation of a sufficiently large pool of scientific experts at the local level. Mirova is supportive of this flexible approach provided that robust, science-based, necessary “checks and balances” are in place to ensure the long-term integrity of the biodiversity credits/certificates.

Effective methodologies should also clarify how and when to bundle biodiversity credits with carbon credits and offer insights into selling them as integrated or distinct units. High-integrity projects must demonstrate financial additional, while still allowing project developers to craft the appropriate revenue strategy for their unique needs.

Regarding safeguards, the Global Biodiversity Framework extensively highlights the importance of Indigenous Peoples and Local Communities (IPLC), including that they should at a minimum benefit from financial flows for nature, as is their right with respect to their territories and efforts. It is important to note that such communities may not want or prefer biodiversity credits as a solution, and that they have the right to decide if and how they are involved. Biodiversity credits have been proposed, and are increasingly being piloted, as a market-based mechanism to help halt and reverse global biodiversity loss. IPLCs are on the frontline to protect and maintain the local ecosystems. When it comes to the development of new markets for biodiversity credits, IPLCs are key stakeholders without whom the market cannot progress. A fair and sustainable biodiversity credits market would take into account the rights of IPLCs, increasingly recognized as the most effective gatekeepers of biodiversity. This includes requiring an agreed share of any revenues from schemes in both primary and, where instituted, secondary markets.

Conclusion: Proceeding in the fog

As a mission-driven company3, Mirova has always explored innovative financing instruments to contribute to the development of a fair and sustainable economic model. Our position is that voluntary markets can unlock innovative funding for robust projects that bear positive and measurable effects on climate and biodiversity while simultaneously addressing social challenges.

Nevertheless, to avoid greenwashing and negative incentive/risk of maintaining business as usual, strict safeguards and governance must be set to ensure a strong integrity of such environmental market instruments. This model would also contribute to scaling up financing for nature-positive projects which, for the time being, remains limited compared to overall private financial flows to developing and emerging markets.

This approach seems already well-understood and initiatives such as ICVCM or IAPB show strong interest from high institutional and governmental levels to address the issue.

While markets are being shaped and structured in real time, we believe action remains critical to obtain concrete results on the ground and can actually contribute to market structuration, as previously seen in other areas such as green bonds.

That is why, faithful to its innovative nature, Mirova will proceed despite the current fog to scout new investment territories, test-and-learn and share best practices for environmental market instruments such as carbon and biodiversity credits, thus contributing to common knowledge and future standards and supporting robust climate and nature positive projects.

1 The disclosure of the recourse to voluntary carbon credits is now part of the CSRD. For more information, please refer to European Sustainability Reporting Standards E1 standard for climate change.

2 Article 6 of the Paris Agreement sets out how countries can pursue voluntary cooperation to reach their climate targets. It enables international cooperation to tackle climate change and unlock financial support for developing countries. Article 6.4 of the Paris Agreement established a new international carbon crediting mechanism. More information here.

3 Introduced in France in 2018 under the Pacte Law, a ‘société à mission’ company must define its "raison d'être" and one or more social, societal or environmental objectives beyond profit. The purpose, and objectives aligned with this purpose, must be set out in its Articles of Association. The Articles specify the means by which the execution of the Mission will be monitored by a Mission Committee (a corporate body distinct from the board of directors which is responsible for monitoring the implementation of the mission with at least one employee.) An independent third party then verifies the execution of the Mission, via a written opinion which is annexed to the report of the Mission Committee to shareholders and made available on the website of the company for a period of five years.

The data presented reflect Mirova’s opinion and the situation at the date of this document and may change without notice.